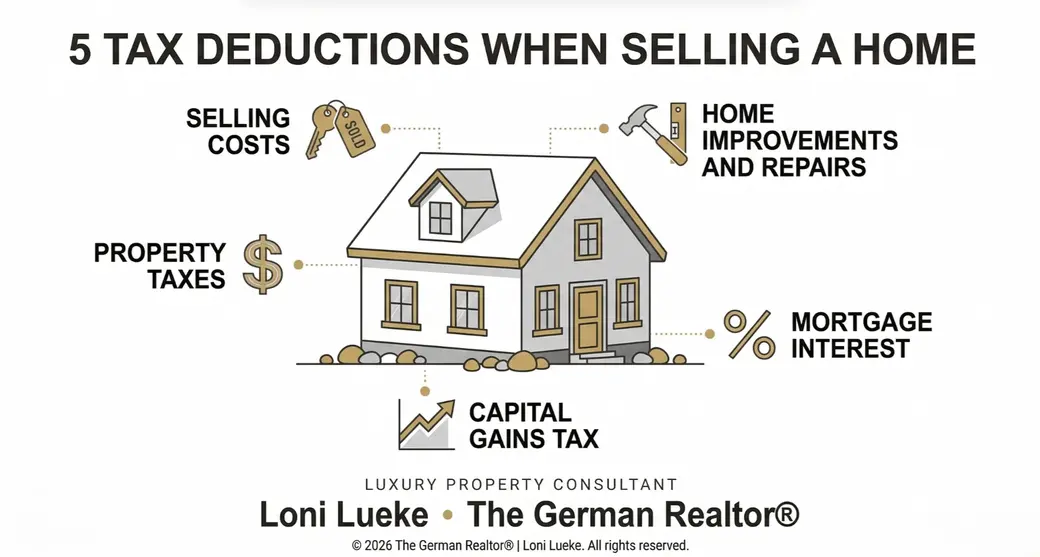

5 Tax Deductions That Can Save You Money When You Sell Your Home

Most homeowners spend months preparing their home for sale. Very few spend time preparing for the tax side of it.

That gap is where money gets left on the table. Selling a home is one of the largest financial transactions most people will ever make, and the tax implications are significant. But the good news is that the tax code offers meaningful deductions and exclusions for sellers who know where to look and keep the right records along the way.

You should always work with a trusted tax professional on your specific situation. What I can do is help you understand how the selling side of the equation works so you walk into that conversation prepared and confident.

The Deductions Every Home Seller Should Know

1. Selling Costs

The costs you pay to sell your home are generally deductible because they reduce your net proceeds and therefore your taxable gain. These include real estate commissions, attorney fees, title insurance, transfer taxes, and staging or advertising costs directly related to the sale.

Many sellers overlook these entirely or lose track of receipts over the years. Keep a folder, physical or digital, for every expense connected to your sale from the moment you decide to list.

2. Home Improvements and Repairs

Capital improvements you made during your ownership can be added to your cost basis, which reduces your taxable gain when you sell. This is one of the most valuable and most underutilized strategies available to homeowners.

The distinction matters here. Repairs maintain your home's condition and are generally not added to your basis. Improvements that add value, extend the home's life, or adapt it to new uses, a new roof, a kitchen renovation, a deck addition, do qualify. Keep every receipt, permit, and contractor invoice from the day you buy.

3. Property Taxes

Property taxes you paid during the year of the sale may be deductible on your federal return, subject to the current SALT deduction limits. The deduction is prorated based on the portion of the year you owned the home before closing.

This is a detail that often gets missed in the paperwork of a sale. Your settlement statement will show the property tax proration, and your tax professional will need that figure.

4. Mortgage Interest

If you carried a mortgage on the home you are selling, the interest you paid during the tax year is generally deductible up to the applicable limits. For most sellers, this applies to the months leading up to the closing date.

This deduction applies to your primary residence and, in many cases, a second home as well, which is relevant for the many Hilton Head owners who carry financing on a vacation or investment property.

5. Capital Gains Tax Exclusion

This is not a deduction in the traditional sense, but it is the most powerful tax benefit available to home sellers and deserves a clear explanation.

If you have lived in your home as your primary residence for at least two of the last five years, you may exclude up to $250,000 of gain from your taxable income as a single filer, or up to $500,000 as a married couple filing jointly. For many homeowners, this exclusion eliminates the capital gains tax liability entirely.

Key qualifications to keep in mind:

- The two-year residency requirement does not need to be continuous

- The exclusion can only be used once every two years

- Second homes and investment properties do not qualify for this exclusion without meeting the residency test

The Strategy That Makes the Biggest Difference

Knowing these deductions exists is only half the equation. The other half is documentation. Here is what every homeowner should keep on file regardless of when they plan to sell:

- Original purchase documents and closing statement

- Records of every capital improvement with dates, costs, and contractor details

- Annual property tax statements

- Mortgage interest statements from your lender

- Any permits pulled for renovation or construction work

The sellers who walk away with the most money are rarely the ones who found a last-minute deal. They are the ones who kept clean records and worked with the right people from the start.

Thinking About Selling Your Hilton Head Home?

Whether you are just beginning to consider a sale or ready to move forward, having a clear picture of both the market value and the financial strategy behind your sale puts you in the strongest possible position.

Send me a message and let's talk through your goals, your timeline, and what your Hilton Head property could mean for your financial future.

Recent Posts